Important Things to Know about Doctor / Physician Mortgage Loans in Illinois and Student Debt

Congratulations Doctor! You’ve completed medical school, earned the degree and are heading into residency in Illinois. If you’re considering buying a local, convenient home near the hospital to live in during your residency, you’re not alone. Interest in homeownership for many in your position usually is highest during this transition period from medical school into a residency. This is an exciting time to be sure as you embark on this next phase.

While most medical students rarely have the income or credit history to buy a home during med school, at 12pm ET on the third Friday in March, Match Day, you find out exactly where you’ll be living for the next 3–7 years and knowing that serves as one of the primary catalysts for home-buying interest. Very soon after that you’ll receive your formal offer with your salary.

So how can you get a jump on this before the best homes are taken? Lenders require proof of income to qualify for a loan. However, certain lenders allow graduating med students to use their signed residency contract as proof of future earnings, allowing them to close on a home up to 90 days before they actually receive their first paycheck.

A quick word about (my) being a broker licensed to originate mortgage loans in Illinois. Banks and direct lenders have their own individual programs and if you don’t fit into their established criteria, they’ll send you back out on the street shopping for a loan.

A mortgage broker has more options for you than a bank or direct lender has because brokers partner with many different wholesale lenders. A broker can search and review many options to find a program that fits with your needs and goals, all in one stop. Whether or not your residency is in Illinois, I work for a national company who is the #1 pure broker in the US so if you contact me, I can refer you to a top broker licensed in your state of residency.

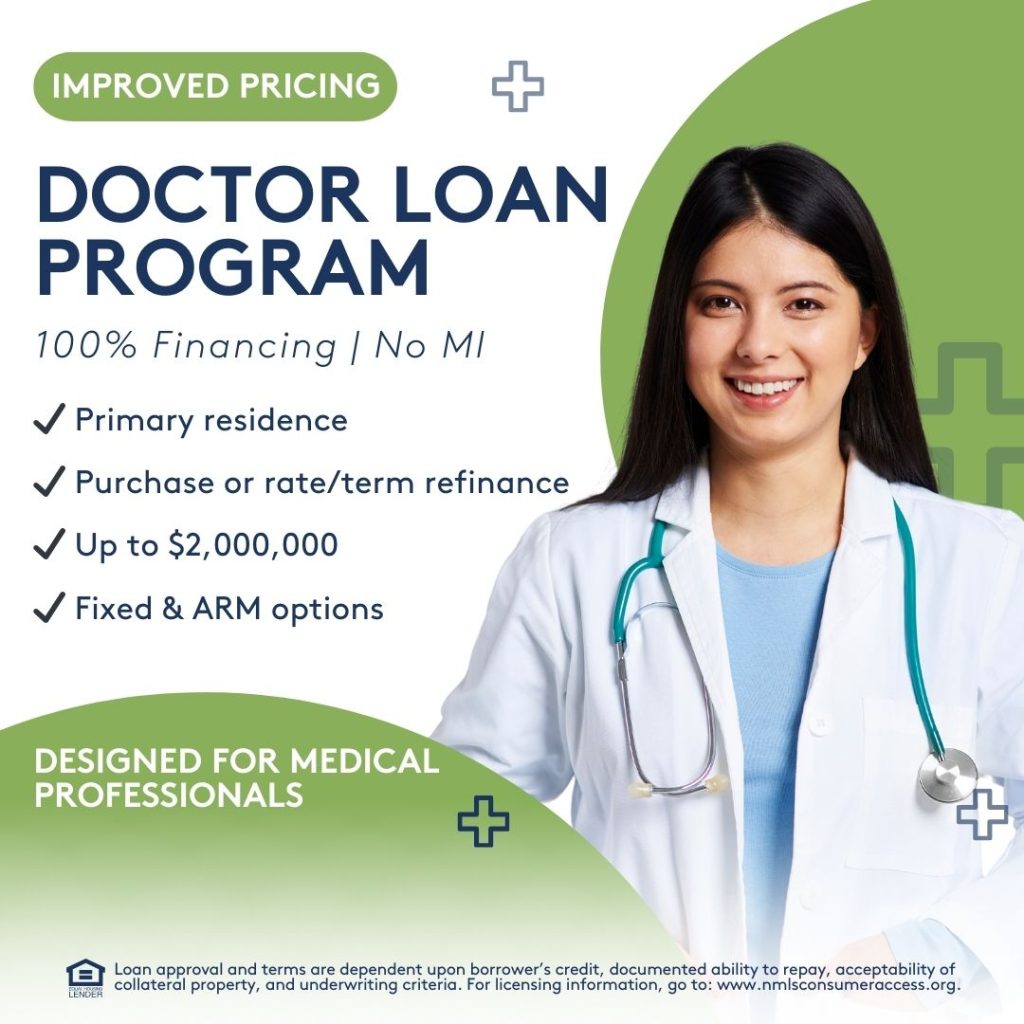

Understanding Physician Loan Guidelines in Illinois

- Need to have an MD, DO, DDS, DMD, PharmD, DVM, VMD, DPM or CRNA.

- Need fully executed employment contract or offer letter

- Loan periods are 15, 20, 25 and 30 year

- There are ARM products available also, some programs require an ARM

- Must be a 1-unit or single family and be your primary residence

- FICO score should be 680 minimum. Lower than this and the restrictions become tighter.

- Minimum Loan Amount is $100,000 or $350,000 for an ARM

- With certain conditions, Student Loan payments that are in deferment, forbearance, or reporting as $0 due to an Income-Based Repayment (IBR) plan may be excluded from the borrowers DTI. Does the initial 6-month grace period on federal student loans count as deferment under the student loan payment exclusion criteria for medical residents and fellows? Yes it does.

- Zero down payment required on many programs

- No Private Mortgage Insurance required

- Gift funds are allowed with no limit

Ready to get started? Let’s Roll. Click on the Apply Now button and complete your application.